Successful physicians often build financial complexity as quickly as they build their careers. Discover why coordinated planning across taxes, investments, practice ownership, estate planning, and long-term goals becomes increasingly important as success evolves.

Many successful women are managing more than wealth. Learn how coordinated planning can help support evolving goals, responsibilities, and opportunities.

Selling a business is often one of life's biggest financial events. Learn why many business owners regret their exit and how thoughtful planning may help.

Artificial intelligence, inflation, interest rates, and shifting market dynamics continue to shape the investment landscape. In this month's RiskBridge CIO Chartbook, we explore the key trends influencing markets, the outlook for economic growth, and why portfolio diversification may look different moving forward.

If tomorrow never comes, would your family know what to do? Family preparedness is about more than legal documents. It's about helping the people you love understand where to turn, who to call, and how to navigate the responsibilities you've spent a lifetime building. Thoughtful preparation today may help reduce stress and confusion when it matters most.

Many successful families quietly reach a point where the planning structures that once supported their success no longer fully reflect the complexity of their lives today.

Financial confidence often begins at home. During Women’s History Month, we reflect on the role families play in teaching the next generation of women about money.

Recent economic indicators suggest a shifting environment for business owners and leaders. From hiring trends to manufacturing activity and investor sentiment, these signals may influence hiring decisions, capital planning, and long-term strategy.

During Women’s History Month, we recognize the growing role of women in wealth management and celebrate the women of Finley Davis Private Wealth who contribute across every part of the client experience.

For families with significant wealth, the challenge in wealth transfer is not simply moving assets, but balancing structure and flexibility. Explore how thoughtful planning can help support the next generation while preserving long-term family intentions.

A pivotal year is approaching for significant-wealth families. Explore 2026 family office opportunities and how Finley Davis Private Wealth may support long-term planning and investment structure discussions.

The latest Business Edge report explores how business owners can interpret market signals even when official government data is limited. Drawing on insights from the RiskBridge CIO Chartbook, Finley Davis Private Wealth highlights five key indicators shaping the outlook for growth, inflation, liquidity, and corporate earnings as the year comes to a close.

Managing wealth across generations can be challenging. At Finley Davis Private Wealth, we help families bridge the investment gap between preserving legacy and embracing innovation.

The world is changing fast. Technology, demographics, and inflation trends may reshape markets. See how Finley Davis helps clients adapt and seek opportunity.

Family offices are built to serve today’s needs, but generational transitions can expose gaps in governance, values, and planning. As the Great Wealth Transfer accelerates, Finley Davis Private Wealth helps families prepare for smooth transitions, align legacy goals, and build structures that evolve across generations.

Even the most experienced families can face costly surprises when financial decisions are made in isolation. This article explores the financial blindspot: how tax, legal, investment, and philanthropic strategies may look solid on their own, but fall short when not fully aligned. Learn how ultra-high-net-worth families can benefit from timely, integrated advice that brings clarity, coordination, and greater long-term impact.

Many UHNW families rely on outdated strategies. This article explores why asset protection for UHNW families is getting more complex, and what modern tools may help reduce risk.

The latest RiskBridge CIO Chartbook is now available, along with a concise video briefing from CIO Bill Kennedy. He shares timely insights on the slowing economy, potential Fed rate cuts, global inflation trends, and where RiskBridge sees opportunities taking shape.

Watch the full video and download the chartbook to stay informed on what’s moving the markets.

Compound planning goes beyond investment returns. By aligning tax, estate, and protection strategies, high-net-worth families may unlock greater financial momentum. Learn how the Finley Davis Rate of Return captures the true value of integrated planning.

Most physicians are sold life insurance as a product, not a strategy.

That’s a problem.

Used the right way, life insurance can support asset protection, supplement retirement income, fund practice transitions, and even offset future tax burdens.

We are almost through what is typically one of the quietest months of the year for US equity volatility (July), with two consistently choppy months ahead (August and October). The VIX peaked in 2025 at 52.3 in early April, a four-standard deviation move, mainly due to the trade wars.

It’s time to think differently about life insurance. Creative strategies may help solve estate taxes, liquidity gaps, and complex legacy planning needs. In the right structure, life insurance can support long-term goals without disrupting your overall plan.

This month’s Business Edge report highlights the latest economic indicators, from payroll gains to shifting sector activity, and what they may mean for your business strategy moving forward.

Life insurance for family offices is often overlooked, yet it may offer essential benefits for ultra-high-net-worth families. Discover how integrating life insurance into your broader wealth strategy could help reduce estate taxes, preserve assets, and support long-term legacy goals.

Market volatility gets a lot of attention, but the greater threat to your legacy may be much quieter. If your estate plan hasn’t been reviewed in years, you could be facing tax exposure, outdated structures, or unintended outcomes. Discover why your estate plan risk deserves a closer look.

Geopolitical tensions are rising, but history shows markets often react differently than headlines suggest. RiskBridge breaks down the current conflict, its market implications, and why this could signal opportunity, not panic.

This summer could test even the most seasoned investors. From debt ceiling volatility to shifting Fed expectations and rising inflation risks, RiskBridge outlines what’s keeping markets on edge and where selective opportunities may lie.

Women often drive the legacy conversation. Explore the emotional side of estate planning and how Finley Davis Private Wealth helps women shape lasting impact.

This month’s Business Edge Report breaks down key economic indicators from June 2025 and explores how they may impact business strategy. Get insights on hiring trends, interest rates, manufacturing activity, and what to watch for in the months ahead.

As financial conditions tighten in today’s volatile markets, many business owners are facing unexpected obstacles, from stricter lending standards to tariff-related disruptions. Learn how these shifts may impact your next move and why proactive business planning matters now more than ever.

The latest CIO Chartbook from RiskBridge dives into the market’s shifting landscape—from rising interest rates and cautious equity positioning to liquidity concerns and global currency movements. Discover what these signals could mean for your investment strategy.

Learn strategies for helping to protect personal wealth from business risks, including shielding assets through LLCs, trusts, and proper entity structuring.

Slower job growth, a stabilizing yield curve, and shifting investor sentiment are all pointing to changes beneath the surface. This month's Business Edge Report breaks down what these signals could mean for your business strategy.

Women are living longer, taking career breaks, and building wealth—but often pay more in taxes over a lifetime. This blog explores why and offers three smart tax strategies to help women investors keep more of what they earn and strengthen their financial future.

Owning property or investments in your personal name could expose your wealth to legal risk. That’s why more high-net-worth individuals are turning to LLCs—not for business, but for personal asset protection. Learn how this overlooked strategy could help shield your wealth and support smarter estate planning.

The first months of 2025 delivered a masterclass in policy-driven market volatility. From unexpected tariff reversals to foreign investor skepticism, this RiskBridge commentary offers insight into what today’s turbulence can teach us about tomorrow’s investment strategy.

As your net worth grows, so do the risks. Private Placement Life Insurance (PPLI) offers high-net-worth individuals a discreet, powerful way to help reduce tax exposure, enhance privacy, and protect assets for the next generation.

Staying invested matters. Missing just a few of the market’s best days can significantly reduce your returns over time. Long-term discipline often beats short-term timing.

When it comes to investing, patience pays. A $10,000 investment in the S&P 500 over 20 years grew to more than $64,000 when left untouched. But missing just a handful of the market’s best days drastically reduced those gains. Trying to time the market often does more harm than good—staying consistently invested through market cycles leads to better outcomes in the long run.

Shield your success. An irrevocable trust can offer powerful protection from lawsuits, creditors, and unexpected risks—going beyond what insurance alone can do.

Think you’re paying too much in taxes? You might be.

Discover advanced strategies to help reduce your tax burden, protect your wealth, and position your assets for long-term success.

As a high-net-worth business owner or investor, you’ve built something valuable. But every April, the reality sets in: Taxes are one of your biggest expenses. The ultra-wealthy don’t just accept high tax bills—they plan proactively to help minimize them.

For business owners and high-net-worth investors, tax season often feels like watching money disappear into thin air. You’ve built significant wealth, made strategic investments, and taken calculated risks—so why does it seem like the IRS is your biggest business partner?

Women control more wealth than ever before—expected to manage $30 trillion in assets by 2030—yet traditional investing strategies have often been built around models that don’t always align with the unique priorities of women investors.

You’ve spent years building your wealth, and along the way, you’ve likely acquired fine art, rare wines, vintage cars, or luxury collectibles—not just for their beauty or history, but because they reflect your passion and personal taste.

For decades, high-net-worth investors have relied on a core portfolio of stocks, bonds, and cash to build and preserve wealth. These traditional investments remain essential, but as market conditions evolve, many investors are seeking ways to enhance diversification, reduce volatility, and unlock new growth opportunities.

Succession planning is more than just preparing for the future of your business—it’s about preserving your legacy and transforming years of hard work into lasting wealth for your family.

Traditional irrevocable trusts offered asset protection but often came with limitations—such as loss of control and restricted access to funds. Modern self-settled trusts overcome these barriers, offering physicians both protection and financial flexibility.

At Finley Davis Financial, we’ve noticed a trend: many high-net-worth individuals don’t ask the right questions about their wealth. Standard wealth management often covers the basics but misses critical topics that safeguard futures and preserve legacies. In today’s fast-changing financial world, skipping these discussions can expose families to unnecessary risks.

The investment world is changing as high-net-worth women lead in luxury real estate. These women are reshaping wealth management. For them, investing goes beyond returns. It's about aligning wealth with values and lifestyle. Understanding their motivations offers insights into the future of wealth management.

The start of a new year is often a time for reflection and renewal. For high-net-worth individuals (HNWIs), it’s also an opportunity to reassess financial goals, fine-tune investment strategies, and ensure that their wealth is aligned with their vision for the future.

Reflecting on 2024 / Looking Ahead to 2025

We reflect on a year shaped by resilience, uncertainty, and innovation. Market trends highlighted economic recovery amidst global challenges, rising adoption of transformative technologies like AI, and shifting policy landscapes.

This December, markets are buzzing with shifts that could significantly impact your business, from strong equity performance to anticipated interest rate cuts and evolving global trade policies.

While celebrating successes is important, as the year draws to a close, this is the perfect time to ask a critical question: Is your wealth truly protected?

As the year winds down, life often feels like a balancing act. Between managing professional responsibilities, family commitments, and personal goals, financial planning can easily slip to the bottom of your priority list. Yet, year-end tax planning is a crucial step in protecting your private wealth and setting the stage for future success.

As a successful woman investor, you’ve worked hard to build your wealth and secure your financial future. With the success you've achieved comes the importance of safeguarding your financial future.

When it comes to building a lasting legacy, strategic financial planning isn’t just about giving—it’s about positioning your wealth to drive long-term value for both family and the causes that matter to you.

In the world of private wealth management, wealth transfer is about more than handing down assets; it’s about creating a legacy built on values, knowledge, and financial responsibility.

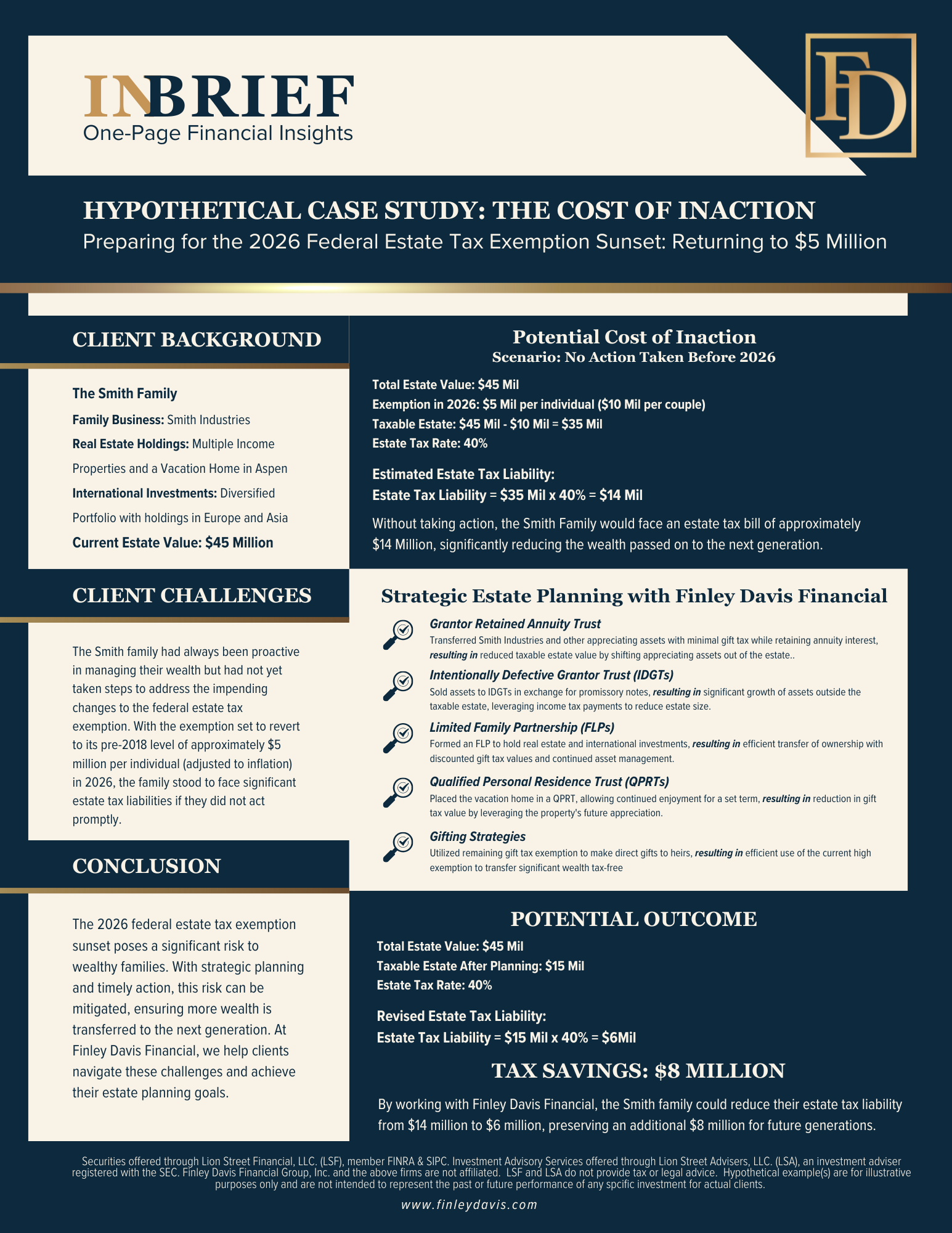

For families with generational wealth, estate planning conversations are essential but often delicate. With the 2026 estate tax exemption sunset on the horizon, addressing these key topics now is essential to preserving your family’s legacy.

Major changes are coming to estate taxes, and they could drastically impact the wealth you pass to your heirs. With the exemption set to drop in 2026, high-net-worth families could face significant tax liabilities—unless proactive steps are taken now.

As we head into another election cycle, the political uncertainty can leave many investors questioning their financial future. But history shows that a divided Congress may actually benefit the markets—bringing stability when you need it most.

Just like sailing a boat through rough seas, managing your investments during election season requires a steady hand. Stay invested. Stay on course. Your future depends on it.

In a world where laws and tax policies are constantly changing, the security of your family’s future can feel uncertain. But with the right plan in place, the legacy you've built will continue to support and inspire the generations that follow.

As you approach retirement, the stakes are higher than ever. The shift from accumulating wealth to preserving and utilizing it requires a carefully crafted strategy that balances growth with stability.

From the threat of malpractice lawsuits to the intricacies of managing high income and taxes, physicians face a range of risks that can jeopardize both their professional and personal financial well-being.

If you have a certain type of life insurance policy, you may be able to sell it for money that you can use now. Learn how a life settlement can help you.

If you maintain a life insurance policy, income will be provided to your loved ones when you pass away. In America, slightly more than half of adults carry life insurance.

Without a proficient team working together toward a common goal, your estate complexities can become overwhelming. It is imperative that all members of your estate team—wealth managers, tax professionals, and legal experts—collaborate effectively, ensuring that your voice and vision are consistently represented.

With the impending changes to the Federal Estate Tax, many families will struggle to find effective solutions that preserve their wealth for future generations. What if more of your money could go where you want it to go—towards your heirs and cherished charitable causes—rather than being lost to taxes?

A corporate trustee is a financial institution or trust company that serves as the trustee for your estate, providing professional management and oversight.